# Spending bitcoin with non-custodial EMV

Abusing the Visa&Mastercard protocol to sign UTXOs with no privkey exposure

---

### [silur@hcpp.cz ~]$ whoami

- Hacker @ 0.0.0.0/0

- Cryptographer @ QANPlatform, CasperLabs, MTA Wigner and others

- Blockchain architect&consultant

- Bug bounty hunter

- Malware analyst

---

## Agenda

- An ancient problem - credit cards & bitcoin

- HW wallets and compatibility

- EMV history

- EMV Protocol overview

- Attack assumptions

- Abuse of protocol for BTC

---

## Only 1% of the population own coins

- Most end-users are dumb for new tech

- UX of btc is **great**, decentralized thinking is the hard part

- Backward-compatibility usually helps with tech but not so easy with crypto

---

## Not so clever plays (personal bias alert)

- Stablecoins :poop:

- App-only banks "supporting" crypto

- Spend-fiat, exchange crypto after settlement interval

- Real-time fiat exchange in custodial wallets

---

## More clever plays

- HW wallets like Trezor, Ledger

- But they need separate apps, APIs

- (e)Commerce can't keep up with new stuff

- Some HW hacks have been introduced recently

- Exotic operations are not possible (no monero stealth support)

---

## My favorite hardware for security:

---

## Why?

- I don't know of any recent CC hacks on hardware level

- Backward-compatible

- Intuitive to most people (2.5 Billion cards out there.. excluding the US!)

- Affordable compared to Ledger and friends

- Support fun crypto like AES256, SHA256, and EC arithmetics generalized to GFp (support curve25519), stealth addrs, maybe even bulletproofs

---

## Requirements of this talk

- Standard, commercially available JCOP card

- Private key stays on the card, signs in place

- Reader/terminal is unmodified

- The tech does not imply fiat in the process (legal part might do)

---

## Equipment?

---

## Remember Max Butler & Friends?

- After CardingForums, Ic3man, Script and other carding gods, EMV came into play

- Europay + Mastercard + Visa

- Flexible, secure protocol for payment

- Channel-agnostic (physical reader or NFC)

- Carding came to a halt (or at least slowed down)

---

## TL;DR EMV - important fields

- Most fields use ASN.1 BER format

- ATC - 16bit counter that the card and the issuer both increment with every TX

- AID = RID + PIX app id

- PDOL - processing options data list

- Issuer certificate & "contact info" in x509

- TVR - 8-bit end result of the transaction

---

## TL;DR EMV - communication

- Uses standard T0 APDU format:

```ascii

[CLA][INS][P1][P2][P3]

| |

class instruction

```

---

## Step 1 - Select app

- ... not really useful because 99% of banks issue only one app (that you actually use)

- We can make coin/wallet-specific slots here, each with their own files

---

## Step 2 - getProcessingOptions

- This is the first operation that increments the ATC so take care when testing

- Provides the PDOL to the reader which will determine our processing decision tree later

---

## Step 3 - read app data

- Interestingly you cannot specify which files to read, it's all-or-nothing so encrypt well...

- Which we thankfully support on the card (AES256, even ECIES)

---

## Step 4 - check 1

- based on the provided app data (expiry, app versions) mask (binary OR) some TRV bits

- ODA auth - shortly verify the certificate chain and crypto signature of the card issuer

---

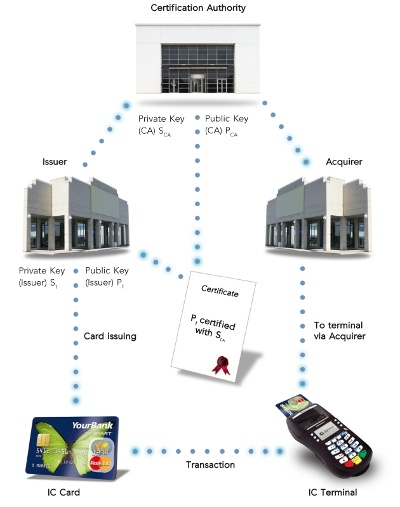

## CA you say?

---

## Not only banks can self-sign certs

- Several airline loyalty cards - https://cards.barclaycardus.com/cards/barclaycard-arrival-plus-world-elite-mastercard.html

- Disney - https://creditcards.chase.com/credit-cards/disney-premier

- Travel agencies - https://www.citi.com/credit-cards/credit-card-details/citi.action?ID=expedia-rewards

- Sports events & programs - https://www.discover.com/credit-cards/cash-back/nhl-card.html

---

## Step 5 - check 2

Cardholder verification either with:

- Cryptographic Signature

- Offline plaintext PIN

- Offline enciphered PIN ( EU )

- Offline plaintext PIN + signature

- Offline enciphered PIN + signature

---

## Step 6 risk management

- Reader & card must aggree on whether continue online or offline

- Reader has more power

- only a small number of offline ATC increments can be made

- This is the part where ATC mismatch result in card blocks and fraud response

---

## Step 7 - send transaction online

- Thankfully the send endpoint is stored on the card as an AFL - we can set up our own backend

- Transactions are packed into a so-called ARQC which is basically the description what we pay for and how much

- **ARQC has no specified format**

- ... so it can be an UTXO!

---

## Step 8 - optional second card action

... basically callbacks with AFL fields to send back to the bank

---

## Step 9 - process scripts

- The ARPC (ARQC response) can have arbitrary, encrypted script to be run on the chip card, undreadable to the reader

---

## The attack:

Assumptions:

- We are signed by a CA (otherwise you are committing CC fraud :)

- We have a synced full node

- We'll use online auth to support ATMs too

- We don't care how the settlement interval is closed (for legal reasons :)

---

- Issuer info is stored on the card

- Acquirer communicates with this issuer

- No technical restriction to make your backend

---

- The card stores the xpub + the UTXO list (these cards have 144kb memory)

- Meanin spends outside of the card breaks it (just like the standard ATC)

- getProcessingOptions should return an Online verification + PIN

- the ARQC is formatted as the signed UTXO which the acquirer forwards to the issuer (us)

- We validate the signature and the transaction sanity

- Forward ARPC trough the acquirer with the new UTXOs as a script

- **Whatever the issuer claims here is unquestioned truth**

---

- At this point, both the card and the reader/terminal have done it's risk management steps, the issuer have the final say on the TX validity.

- Scripts can be arbitrary javacard code, we can store our UTXOs or even replace keys

---

## Settlement?

- Usually a 5-7 day interval

- .. but banks use legacy software, it's much more chaotic

- You don't get a CA signature without due diligence

- But self-signing is not that hard (much easier than getting money transmit etc licenses)

---

## An extra assumption

IF we modify the reader side we can eliminate the settlement issue with mastercard with a separate app besides the unmodified MC AID.

---

## Thanks

Also thanks for Max Hillebrand for pointing out some issues with this attack \o

silur@cryptall.co

@Huohuli

{"metaMigratedAt":"2023-06-15T13:34:59.074Z","metaMigratedFrom":"Content","title":"Spending bitcoin with non-custodial EMV","breaks":true,"contributors":"[{\"id\":\"f4d4af67-750e-4c99-b33e-c04b6d99a6c6\",\"add\":7054,\"del\":69}]"}